8 Alternatives to a Credit Card Cash Advance

When you require cash fast, your initial idea could be to count on a credit card cash loan. It fasts, it’s very easy, and also often your credit card issuer appears to be begging you to borrow by sending you offers and also blank checks. Still, cash loan carry lots of expenses as well as restrictions, so before going this route, make certain you examine alternative funding– such as the methods listed here. First, however, let’s analyze the regards to a credit card cash loan, so you can much better contrast it to other choices.

Just How a Charge Card Cash Advance Functions

A charge card cash advance is a money car loan from your charge card provider. As with any kind of acquisition, the cash advance will look like a transaction on your monthly card statement, and interest will certainly build up until it is paid off.

Substantially, however, the terms for cash loan are various from those of daily purchases– and not in your favor. There is typically no grace period for cash advances; the interest starts building up from the purchase day. Additionally, the interest rate is usually rather greater for cash loan than for day-to-day acquisitions.

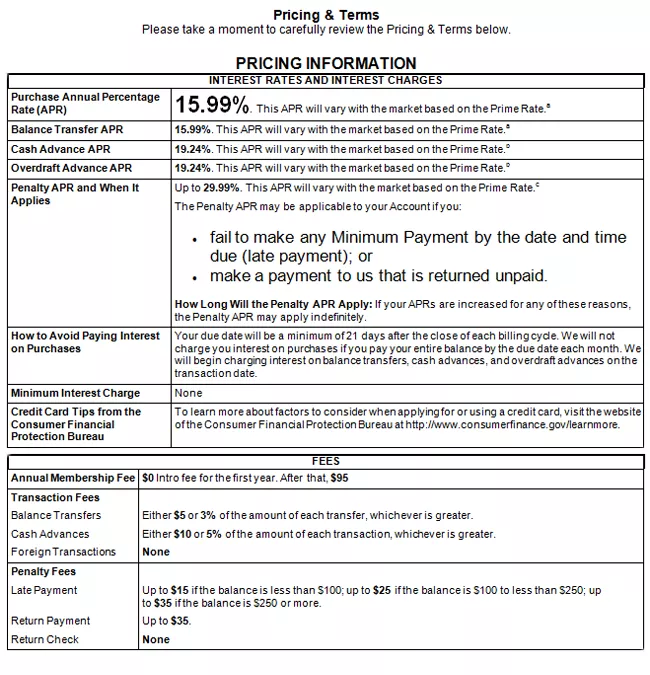

Credit Card Cash Advance Terms

Information concerning cash loan charges and terms can be discovered on the Schumer box for the charge card, which should show up on your card declaration or in the initial bank card agreement. Here’s an instance from the Chase Sapphire Preferred card. It shows that the annual percentage rate (APR) for a cash advance is 24.99%, contrasted to 15.99% for acquisitions (depending upon credit scores). The fee is $10 or 5% of the development, whichever is better.

An additional important detail: When a credit card has different balances, settlements are applied in the way divulged by the charge card issuer, not always to the equilibrium the cardholder wants to pay off initially. For Military Celebrity Incentives account owners, Chase uses the minimum repayment to the balance with the greatest APR. Any type of repayment above the minimum is used “by any means we select.”

These terms suggest that even if you make payments routinely and also vigilantly, it can be tough to settle the development, particularly if you’re remaining to use the card to make acquisitions. Obtaining sucked into an ever-increasing financial debt spiral is extremely simple.

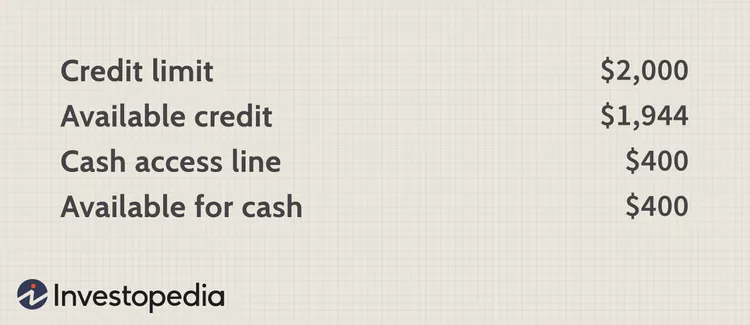

Cash loan are often restricted to a percentage of the cardholder’s credit limit. Each bank card company has its policy and also formula for setting cash advance restrictions. In this instance, the money restriction is 20% of the credit limit:

8 Alternatives to a Bank Card Advance

Because of the higher expense of a cash loan, it’s worth exploring other income resources. Depending on your creditworthiness as well as properties, these 8 alternatives might be far better than or otherwise just as good as a cash advance. Each has advantages and disadvantages.

1. Funding From Friends or Household

Take into consideration asking individuals near to you for a totally free or low-interest short-term finance. Yes, asking can be humiliating, and also the lending can come with a great deal of psychological strings. It will help if you maintain points professional: Make use of a correctly performed written contract that define every one of the terms, so both sides recognize specifically what to anticipate concerning price and also settlement.

2. 401( k) Funding

Many 401( k) administrators enable participants to borrow funds from themselves. Rate of interest and fees differ by company as well as strategy administrator however are generally affordable with dominating personal funding prices (see listed below). The financing limit is 50% of the funds approximately an optimum of $50,000, and repayment is 5 years or less. There is no credit check, as well as payments can be established as automated deductions from the consumer’s incomes. Remember that while you’re obtaining funds from your 401( k), they are not making any kind of investment returns, which might impact your retired life.

COVID-19 Pandemic Exception to 401(k) Loans and Early Withdrawals

There was an exemption made to this lending restriction in 2020 under that year’s Coronavirus Help, Relief, as well as Economic Safety (CARES) Act came on March 2020 in action to the COVID-19 pandemic. Under the CARES Act, 401( k) between March 27 and Sept. 22, 2020, borrowers might get 100% of their 401( k) account, approximately $100,000.

Besides, Congress permitted 401( k) owners to take up to $100,000 in circulations without a hit from the 10% percent very early withdrawal fine for those younger than 59.5 years of ages. If you took distributions early in 2020, you did have to pay earnings tax obligation on the withdrawal. Yet the internal revenue service allowed for a three-year duration of repayment. Indicating you can pay those tax obligations extended over time, or you can pay back the circulation as a rollover contribution.

3. Roth IRA

While it’s not very suggested because the funds are intended to be for retirement, there is a method to utilize your Roth IRA as an emergency fund. Since contributions to a Roth IRA are made with after-tax bucks, Irs (INTERNAL REVENUE SERVICE) regulations permit you to take out that cash any time without penalty as well as without paying extra tax obligation. If you’re under the age of 59 1/2, however, be sure not to withdraw more than you’ve added, even if the account has expanded in size. The revenues on your contributions go through tax obligations and also charges.

4. Financial Institution Personal Lending

For a customer with good or excellent credit report, an individual funding from a financial institution might be less costly than a bank card cash loan. Likewise, the benefit will be quicker than making bank card minimum repayments, better lowering the amount of total rate of interest paid.

5. Collateral Car loan

Any type of financing secured by real properties is a security lending, which usually has less-stringent credit scores requirements than an unprotected loan. House equity loans and lines of credit are protected by your home’s value, for example. Some banks likewise make car loans versus the worth of a count on or certificate of deposit (CD).

6. Wage Breakthrough

Lots of companies offer inexpensive payroll developments as an option to more expensive traditional payday loans. Fees can be as reduced as $8, but beware of rate of interest. They range from 10% to 165%, which is predatory lender territory. Repayments can be set up as automatic income deductions.

7. Peer-to-Peer Financing

P2P financing, as it has come to be known, is a system in which individuals borrow money from investors, not banks. Debt needs are less rigid, and also authorization prices are higher. One of the most costly car loans peak at concerning 30% APR, plus a 5% car loan cost.

8. Cash Advance or Title Financing.

A car title loan should be thought about as a last resource because of its huge expense. Like title financings, cash advance usually charge rates of interest well in the three-way numbers– 300% to 500% as well as even more. The costs on both kinds of lendings can be so expensive for customers strapped for money that several renew their financings a number of times, at an ultimate expense of numerous times the original car loan quantity. These two are probably the only loans that the bank card cash advance is superior to– except in states where the interest rates on this type of financing are capped very stringently.

The Bottom Line

Every temporary finance alternative has its pros and cons. A cash-flow problem is a high-stress situation, however that does not indicate you ought to stress. Require time to think about all your alternatives. The terms for short-term finances are commonly strict, economically in addition to psychologically. Nonetheless, depending upon your specific needs and also schedule, an additional sort of financing might be more suitable to obtaining from your bank card. Charge card cash loan are pricey enough that they ought to just be considered in an authentic emergency situation.